Tesla Stock: Barclays Weighs “Two Contrasting Stories” Ahead of Q3 Earnings

Tesla (NASDAQ:TSLA) has always offered a bit of a schizophrenic investment case.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

On the one hand, most of its revenue to date has been derived from car sales. However, its valuation is nothing like that of other automakers, and that’s where the split personality becomes evident. Indeed, the Elon Musk-led firm is viewed as more of a tech play in the pursuit of advancements in AI, autonomous driving, and robotics.

The dual narrative has become especially pronounced this year, as noted by Barclays analyst Dan Levy ahead of the company’s upcoming Q3 readout scheduled for this Wednesday.

“Tesla enters 3Q earnings with two contrasting ‘stories,’ an accelerating AV/AI narrative bolstered by Elon’s proposed comp package/re-engagement vs. a weakening fundamental backdrop with 3Q deliveries widely expected to be peak volumes for some time,” the analyst said.

The stock has surged more than 30% since early September, fueled by renewed optimism around Musk’s “re-engagement” (including a proposed compensation package that could approach $1 trillion and his recent $1 billion share purchase) as well as solid, though potentially short-lived, Q3 fundamentals due to accelerated purchases thanks to the expiration of the $7,500 EV tax credit in the U.S. on September 30.

Nevertheless, Levy thinks the recent gains have been driven less by near-term fundamentals and more by the broader AV/AI narrative, with investors continuing to see the autonomous and AI opportunity as central to the story – despite the uncertainty around the commercialization timeframe. Although tangible progress on Robotaxi and Optimus remains limited, sentiment has been boosted by the ambitious “Mars-shot” milestones outlined in Musk’s proposed compensation package, which would demand major breakthroughs in AV/AI and a much higher stock price.

At the same time, Levy remarked, “fundamentals don’t matter…until they matter.” Eventually, they will regain importance for Tesla investors, as the core automotive business plays a vital role in financing the company’s longer-term AV/AI ambitions, particularly the “very cash-intensive” process of scaling the robotaxi platform.

Heading into the print, Levy is leaning “neutral to slightly negative.” Amid the recent rally, the analyst thinks the deliveries beat and anticipated strong Q3 results are largely reflected in the current share price, so any mention of weaker near- or mid-term fundamentals beyond the third quarter could weigh on the stock.

“That said, any weakness might be short-lived, as we could subsequently see further excitement building beyond the call into the Nov 6 AGM – which we expect to be a key event reinforcing Tesla’s future growth narrative,” summed up Levy.

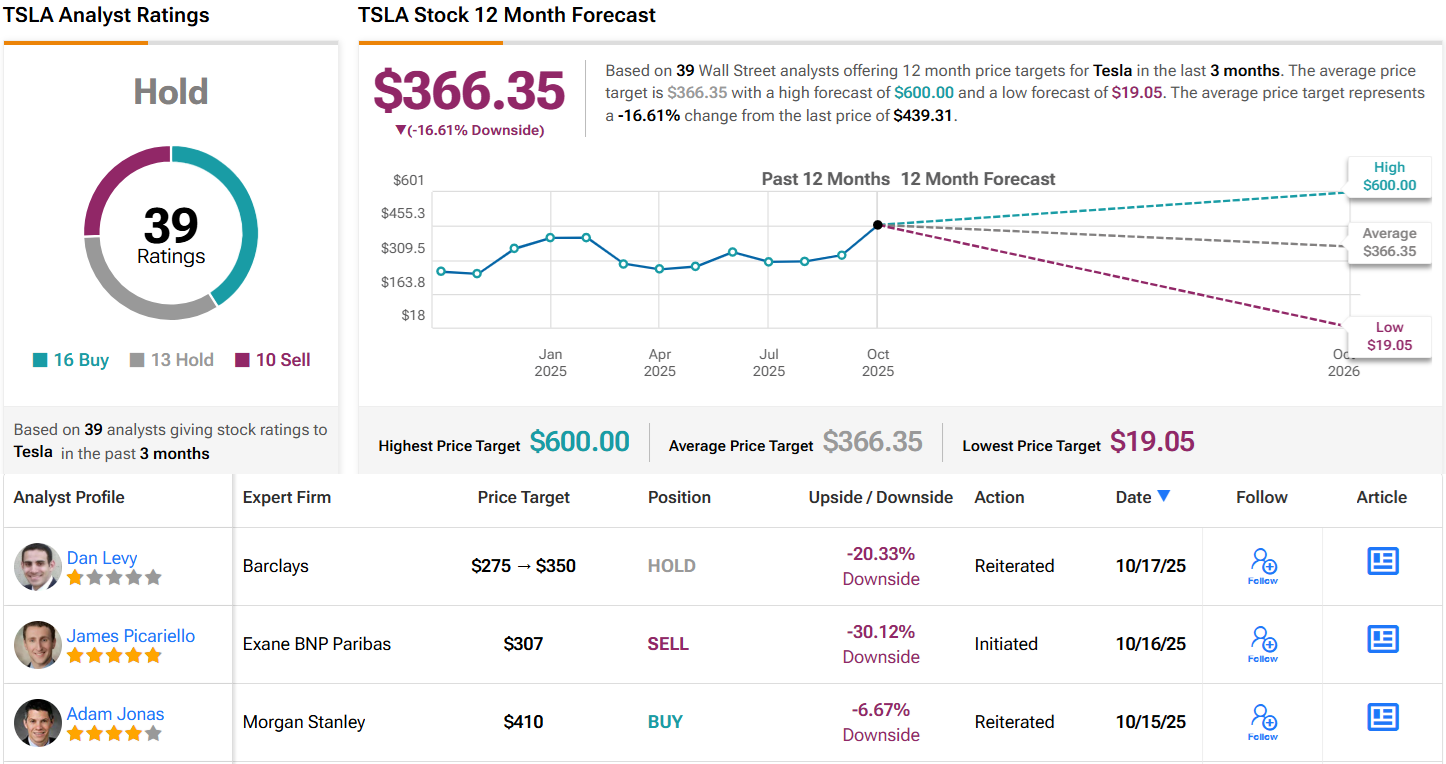

Bottom line, Levy remains on the sidelines, recommending an Equal-Weight (i.e., Neutral) rating, although he is raising his price target from $275 to $350. Still, that figure sits ~20% below the current share price. (To watch Levy’s track record, click here)

Levy’s thesis tracks with the general Street view; the stock claims a Hold consensus rating, based on a mix of 16 Buys, 13 Holds, and 10 Sells. Meanwhile, the $366.35 average target points toward 12-month losses of ~17%. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

First Appeared on

Source link

{kind=link}