The Time Is Right? Here’s What This Top Investor Thinks About Tesla Stock

Tesla, Inc. (NASDAQ:TSLA) finally burst through the wall of disappointing numbers, with a record-breaking quarter of EV deliveries in Q3 2025. The 497,099 EVs represented a company peak, a welcome respite after year-over-year declines in both Q1 and Q2 of 2025.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But while the recent figures were strong indeed, there were some questions regarding how much they truly reflected sustainable growth. After all, the expiring $7,500 EV consumer tax credit offered powerful incentive for would-be buyers to pull their purchases forward into Q3.

That wasn’t the only concern for Tesla bulls, either. Even as revenues increased by 12% year-over-year to $28.1 billion, margins were falling. GAAP gross margin decreased from 19.8% to 18% year-over-year, while GAAP earnings per share fell by 37%.

While happy to acknowledge the company’s strong top-line performance, top investor Daniel Sparks is worried about Tesla’s decreasing margins.

“Third-quarter profitability was more complicated and — unfortunately — not as encouraging,” explains the 5-star investor, who is among the very top 1% of stock pros covered by TipRanks. “The investment question is whether profits can scale as fast as revenue from here.”

Sparks is fully aware that some of the margin deterioration is partly due to increased operating expenses, which increased by 50%, as the company pursued autonomy improvements. In addition, the investor believes that Q3 demonstrated that Tesla has the ability to grow despite macroeconomic uncertainty.

There is also a big opportunity for Tesla’s self-driving (supervised) technology to contribute to earnings, notes Sparks. The investor points out that Tesla’s paid full self-driving customers represent only 12% of its existing vehicle fleet.

“This could move up materially over time, though, especially if the software goes from supervised to truly full self-driving,” adds Sparks.

Still, TSLA is trading at a “lofty” Price-to-Sales multiple, notes the investor. Though software and fleet monetization via robotaxis could make the calculus worthwhile, Sparks also acknowledges the question marks regarding both the timing and the economics of these grand ventures.

Altogether, the high price and the uncertainty add up to a cautious approach from Sparks.

“The valuation arguably prices in too much, leaving little room for error. I’d stay on the sidelines for now,” sums up the investor. (To watch Daniel Sparks’ track record, click here)

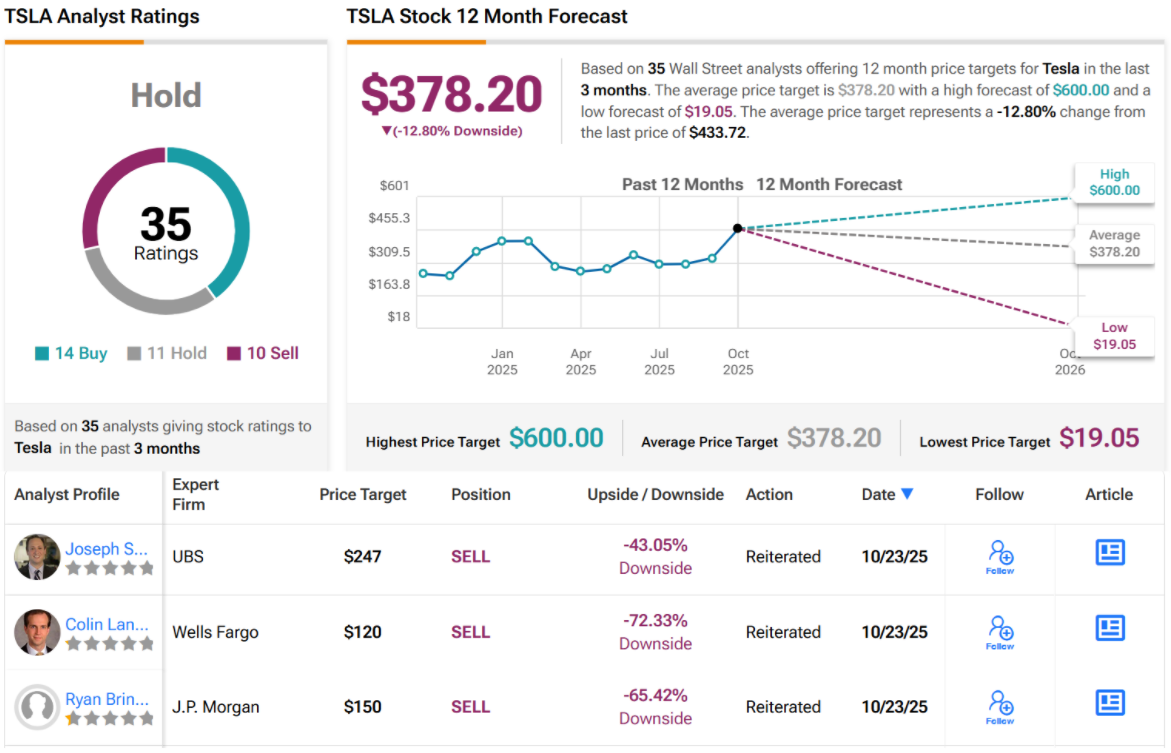

Wall Street is pretty evenly split when it comes to TSLA. With 14 Buys, 11 Holds, and 10 Sells, TSLA carries a consensus Hold (i.e. Neutral) rating. Its 12-month average price target of $378.20 implies losses of ~13%. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

First Appeared on

Source link

{kind=link}