Does Friday’s crash end the debasement trade?

The debasement trade took off after Chair Powell’s dovish keynote speech on August 22 at Jackson Hole. Up until that speech, the Fed had been torn between a weakening labor market on the one hand and above-target inflation on the other. After 100 basis points in cuts in 2024 (including a controversial 50 basis point cut before the election), this had kept the Fed on hold in 2025, which was infuriating Trump.

Powell’s speech was so important because it chose sides, putting a greater weight on the labor market than on inflation. The signal was clear. The Fed would resume rate cuts even though inflation was high. Markets – understandably – wondered if this was happening because of Trump’s constant badgering. The debasement trade was born and precious metals – one particular manifestation of this trade – took off.

On a fundamental level, the nomination of Kevin Warsh changes nothing about any of this. Public debt is high and rising. This pushes up longer-term yields, which makes it inevitable that political pressure on the Fed to cut interest rates and cap longer-term yields will mount. The debasement trade, which is markets searching for safe havens from debt monetization, has a lot further to run no matter who the next Fed Chair is.

This is the big picture. Today’s post makes two additional points, which also say the debasement trade has a lot further to run. First, Friday’s drop in precious metals made it look like markets think Kevin Warsh is a hawk. They don’t. Futures moved to price more rate cuts on Friday, which is fundamentally bullish for the debasement trade. Second, even though Friday’s 26 percent drop in silver and 9 percent drop in gold are bone-jarring, the recent spike in precious metals has been so crazy that this only took gold and silver prices back a few weeks. The debasement trade is very much intact.

The chart above shows tick-by-tick data for the 2-year Treasury yield on Friday. The official announcement that Trump is nominating Warsh came in a Truth Social post at 6:48 am. The 2-year Treasury yield began to fall immediately, rose briefly at 8:30 am when December producer price inflation had a big upside surprise and then resumed its fall into the close. Markets think Warsh will be dovish on interest rates, which is fundamentally bullish for the debasement trade. Indeed, the worst possible nightmare for Warsh must be to have Trump turn on him the way he turned on Powell. The only way to avoid this happening is to cut hard and fast ahead of the midterm elections.

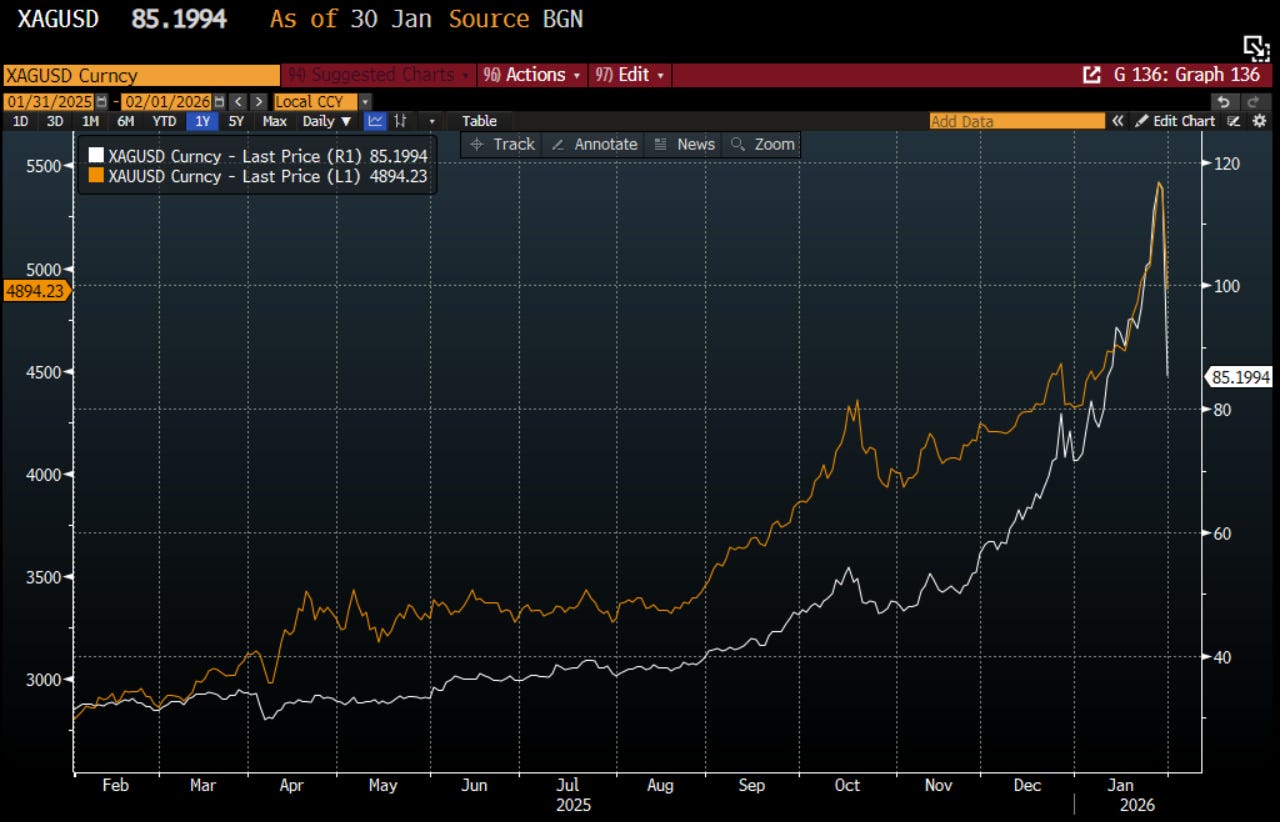

As massive as Friday’s fall in silver and gold prices is, it barely scratches the surface of the run-up in precious metals. The 26 percent drop in silver takes it back to January 12, as the white line in the chart above shows. The nine percent fall in gold merely takes its price back to January 22, as the orange line in the chart above shows. Friday’s correction thus did modest damage to the debasement trade. It’s my expectation that precious metals prices will take off again relatively quickly, like they did after the correction in October.

First Appeared on

Source link