We must explain to you how all seds this mistakens idea off denouncing pleasures and praising pain was born and I will give you a completed accounts off the system and expound

Slate’s Washington, 1707 L St. NW, Washington, D.C., 20036.

(Bloomberg) — Wall Street saw a relief rally as cooler-than-estimated inflation reinforced trader conviction on Federal Reserve interest-rate cuts.

Stocks extended their October advance, with the S&P 500 hitting all-time highs on bets policy easing will power corporate earnings. While the reaction in Treasuries was more subdued, money markets continued to price in a high likelihood of two Fed reductions before the year is over.

Most Read from Bloomberg

Stocks hit all-time highs.Source: Bloomberg

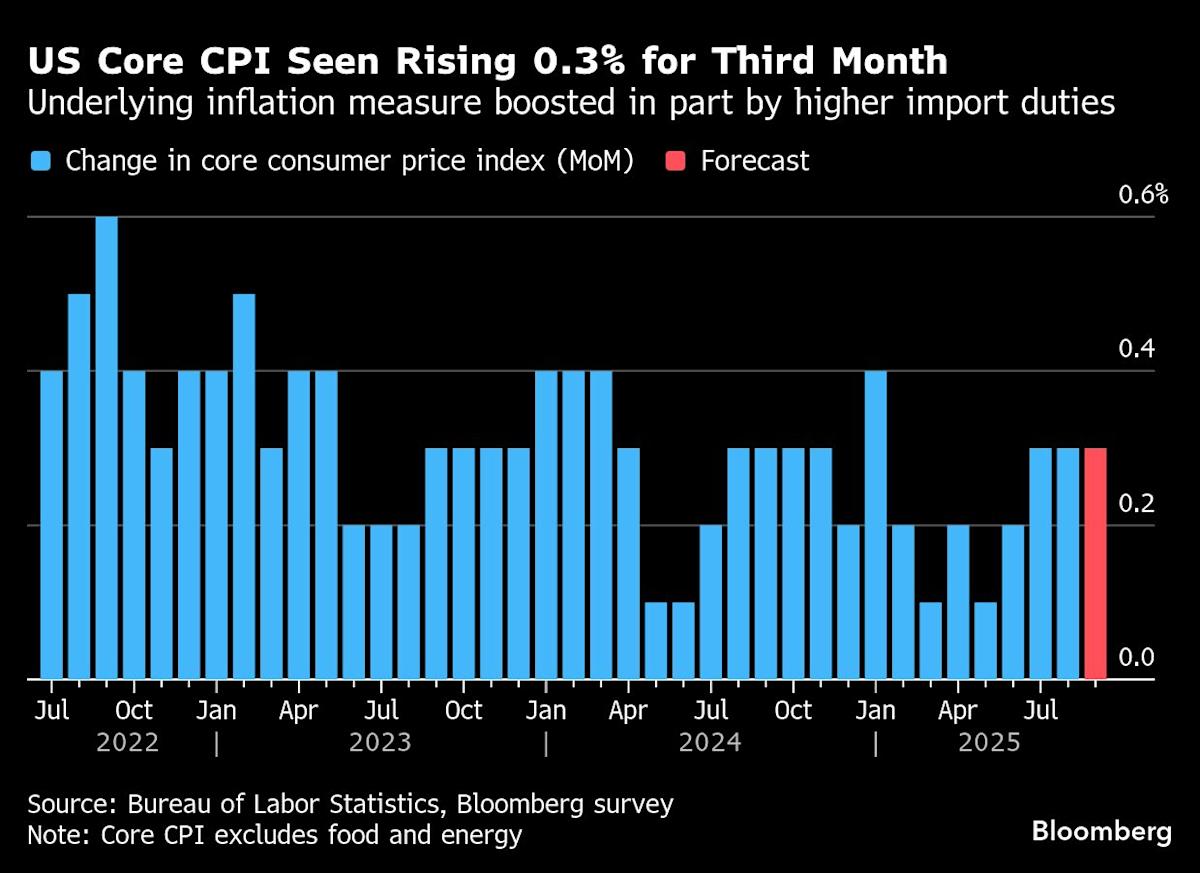

The slowest pace in three months for underlying inflation was welcomed by traders, who’ve been flying almost blind amid the dearth of economic data since the start of the US shutdown. The September core consumer price index increased 0.2% from August. On an annual basis, it rose 3%.

While the Fed was already widely expected to lower borrowing costs next week, the CPI report may help convince policymakers they can do so again in December.

“There was little in today’s benign CPI report to ‘spook’ the Fed, and we continue to expect further easing at next week’s Fed meeting,” said Lindsay Rosner at Goldman Sachs Asset Management. “A December rate cut also remains likely.”

The US government will probably be unable to release inflation data for October, the White House said Friday, citing the ongoing government shutdown.

The S&P 500 rose 1%, topping 6,800. Treasury two-year yields slid one basis point to 3.48%. The dollar wavered.

“Good news on a Friday!” said Art Hogan at B. Riley Wealth. “The Fed has been clear that they are more focused on the softening labor data and will continue to defend their full employment mandate” even with inflation running above target.

“As long as incoming data signal more risk to employment than to inflation, the Fed’s policy path likely points toward additional easing,” said Jason Pride at Glenmede.

The CPI report confirms what we’ve seen overall from private data during the government shutdown — little indication that inflation is surging or that the labor market is falling off a cliff, according to Ellen Zentner at Morgan Stanley Wealth Management.

“For a Fed focused on prudent ‘risk management,’ that should translate into another rate cut next week, and likely more to follow,” she said.

To Bret Kenwell at eToro, it would have taken a shockingly bad report to derail an October rate cut, but at a time when economic data is a bit sparse, investors will take any clarity they can get.

Kenwell also noted that while we may in fact get two more rate cuts this year, the Fed will struggle to justify a more aggressive rate-cutting approach in the face of stubbornly high inflation — unless there’s persistent and notable weakness in the labor market.

“Regardless, stocks can do well in a mild inflationary environment, as we have seen over the past few years. For that to continue, we’ll need to see strong earnings, and so far this earnings season, that’s been the case,” he said.

“Much like a Sherlock Holmes’ story, inflation is the dog that didn’t bark,” said Chris Zaccarelli at Northlight Asset Management. “So many people have been expecting a sharp increase in inflation and have positioned bearishly as a result, but the market is likely to keep squeezing the shorts until they realize that the economy – and Corporate America – is more resilient than many expected.”

Zaccarelli also noted that while equity valuations are high and there are risks in the market, with the Fed cutting rates and corporate profits continuing to increase, it’s hard to see an interruption of this year’s bull market.

“Next year will bring new challenges, but we wouldn’t advise getting in the way of the upward trend between now and year-end,” he said.

Interest-rate swaps signaled traders have all but fully priced in a quarter-point rate cut at the Fed’s meeting next week, followed by another reduction in December.

Overall, the inflation figures locked in a 25 basis-point cut next week and will likely result in a “dovish cut” tone, according to Ian Lyngen at BMO Capital Markets.

“The CPI report leaves an October Fed rate cut a done deal with a December cut also highly likely,” said Oscar Munoz and Gennadiy Goldberg at TD Securities. “However, given that this is priced in, further bullish momentum in rates is likely to be contained.”

With the October cut fully priced in, markets will remain focused on guidance around future rate cuts and the end of quantitative tightening, which the TD Securities strategists expect to be announced at the October meeting.

When Fed officials meet next week to decide whether to cut rates again, they’ll face another question that’s becoming increasingly urgent — how soon they should stop shrinking the bank’s $6.6 trillion portfolio of securities.

Money markets have been flashing warnings for several weeks that the process, known as quantitative tightening, may have run its course. Now, Wall Street strategists say, stress signals have gathered such momentum that the Fed may be forced to end QT as soon as this month.

At JPMorgan Chase & Co., Michael Feroli says he expects the Fed to decide next week to end balance-sheet reduction, or QT.

Feroli also says the case for expecting a cut next week is a simple one: Fed speakers, even some of the more hawkish ones, have done little to push back on the market’s firmly held view that a cut is coming.

He expects the post-meeting statement will be little-changed relative to the September statement. At the press conference, Feroli believes that Chair Jerome Powell will continue to characterize the easing as a risk-management move.

“We don’t anticipate he will signal any bias regarding the December meeting; with potentially three months’ worth of data to be released between now and then, we see little upside from any signaling that could end up being quite improvident,” he said.

Traders are betting that the Fed will cut the rate by a total of 120 basis points over the next 12 months. That would bring benchmark borrowing costs to 2.9%, below the 3% mark — considered a neutral level that neither stimulates nor restricts the economy.

“The data confirms that US inflation remains sticky, but is gradually fading, reinforcing the case for multiple Fed rate cuts into next year,” said Florian Ielpo at Lombard Odier Asset Management.

While signs of tariff-induced inflation are apparent in select categories such as apparel and furniture, goods prices increased at a slower pace in September than August broadly, according to Josh Jamner at ClearBridge Investments.

“This suggests that the pass-through of higher tariffs to consumers has continued to undershoot expectations, which in turn has opened the door for the Fed to lower rates to support a cooling labor market,” he said.

Jeffrey Roach at LPL Financial noted that while tariffs were likely the culprit for rising apparel prices in September, inflation metrics will likely improve by December, setting the Fed up to continue easing throughout 2026.

“Inflation is staying contained at this point,” said Eric Teal at Comerica Wealth Management. “The impact from tariffs has been mostly felt in lower end consumption imports. The current inflation report combined with a weaker job market provides cover for additional rate cuts in 2025 and into next year.”

Overall, this report shows tariff-related price adjustments are more modest because competitive pressures within the retail industry are pushing companies to find other ways to offset the additional costs, according to Tiffany Wilding at Pacific Investment Management Co.

“With inflation expectations still looking anchored, we are not too worried about runaway inflation here despite lingering tariff effects,” said Don Rissmiller at Strategas.

To Scott Helfstein at Global X, the delayed inflation report was not great, but not bad enough to stop the Fed from cutting. Prices have been reasonably stable outside utilities and used cars despite tariffs.

“Yes, prices are higher, but not enough to keep them from helping the economy,” he said. “US consumers do not like higher prices, but are still eating out.”

Separate data showed US consumer sentiment fell in October to a five-month low, as worries persisted about stubbornly high prices and the impact on their finances.

“Today’s numbers help the Fed’s narrative that at least inflation is mostly moving in the right direction,” said John Kerschner at Janus Henderson. “Right now, the markets are seemingly giving the Fed a pass to cut rates through the end of 2025.”

WATCH: Tiffany Wilding at Pimco on CPI.Source: Bloomberg

Corporate Highlights:

Intel Corp. returned to profitability last quarter and gave an upbeat revenue forecast, suggesting that it’s making progress on a long and challenging comeback attempt.

Ford Motor Co. signaled it will largely bounce back next year from a devastating fire that hobbled a key supplier to its top-selling F-150 pickup, sending shares up the most in more than three years while assuaging concerns over one of the automaker’s biggest money-makers.

Procter & Gamble Co. reported better-than-expected sales for its first quarter as consumers brushed off price increases and snapped up its Gillette razors and Secret deodorant. The company also cut its projected impact from tariffs in half.

General Motors Co. cut hundreds of jobs on Friday, just days after raising its profit guidance for the year in a move that sent the shares soaring.

Target Corp. is eliminating about 8% of corporate roles in its first major restructuring in years, according to a memo viewed by Bloomberg News, as the retailer seeks to reduce complexity and regain its footing.

Newmont Corp. is starting to reap the benefits of cost-cutting measures, with the world’s largest gold miner delivering stronger-than-expected quarterly earnings.

Eli Lilly & Co. agreed to buy Adverum Biotechnologies Inc., a company working to treat blindness, in a deal that ultimately could be worth $261.7 million as it continues a push into gene therapies.

JPMorgan Chase & Co. plans to allow institutional clients to use their holdings of Bitcoin and Ether as collateral for loans by the end of the year in a significant deepening of Wall Street’s crypto integration.

Crypto.com became the latest cryptocurrency firm to pursue a US bank charter as it seeks to further its custody-service business for products such as digital-asset treasuries and exchange-traded funds.

Deckers Outdoor Corp., the owner of Hoka running shoes and Ugg boots, forecast 2026 revenue that falls short of analyst expectations, reflecting pressured consumer spending.

Porsche AG suffered its first quarterly loss as a listed company, with the luxury-car manufacturer taking a €3.1 billion ($3.6 billion) hit this year from scaling back its electric ambitions and US tariffs.

WATCH: David Kelly at JPMorgan Asset Management on markets.Source: Bloomberg

Let us know

What Bloomberg Strategists say…

“The 3% CPI print has changed little because the market expects inflation to be around this sort of level for a while as the Fed removes its foot from the brakes. In other words, the market anticipates a Fed that’s turning its attention to the labor-market part of its dual mandate.”

— Sebastian Boyd, Macro Strategist, Markets Live. For the full analysis, click here.

Some of the main moves in markets:

Stocks

The S&P 500 rose 1% as of 2 p.m. New York time

The Nasdaq 100 rose 1.2%

The Dow Jones Industrial Average rose 1.2%

The MSCI World Index rose 0.8%

Bloomberg Magnificent 7 Total Return Index rose 0.9%

The Russell 2000 Index rose 1.5%

Currencies

The Bloomberg Dollar Spot Index was little changed

The euro was little changed at $1.1625

The British pound fell 0.2% to $1.3301

The Japanese yen fell 0.2% to 152.81 per dollar

Cryptocurrencies

Bitcoin rose 0.7% to $110,341.11

Ether rose 1.6% to $3,892.16

Bonds

The yield on 10-year Treasuries declined one basis point to 3.99%

Germany’s 10-year yield advanced four basis points to 2.63%

Britain’s 10-year yield was little changed at 4.43%

The yield on 2-year Treasuries declined one basis point to 3.48%

The yield on 30-year Treasuries was little changed at 4.58%

Commodities

West Texas Intermediate crude fell 0.3% to $61.62 a barrel