The Oil Crisis is About to Get Physical

Source: JP Morgan via Marketwatch

In normal times, about 20 percent of the world’s oil production passes through the Strait of Hormuz. That flow has been cut off except for Iranian oil and a handful of other vessels the Iranians are allowing through. This disruption has led to a large spike in oil futures prices:

Source: Trading Economics

But this price rise has been speculative, driven by the (justified) expectation of future shortages rather than a current lack of oil. In fact, so far deliveries to markets around the world haven’t declined, because shipping oil from the Persian Gulf to major markets takes 4-6 weeks. As a result there was a large quantity of oil already at sea, outside the Strait, when the war began.

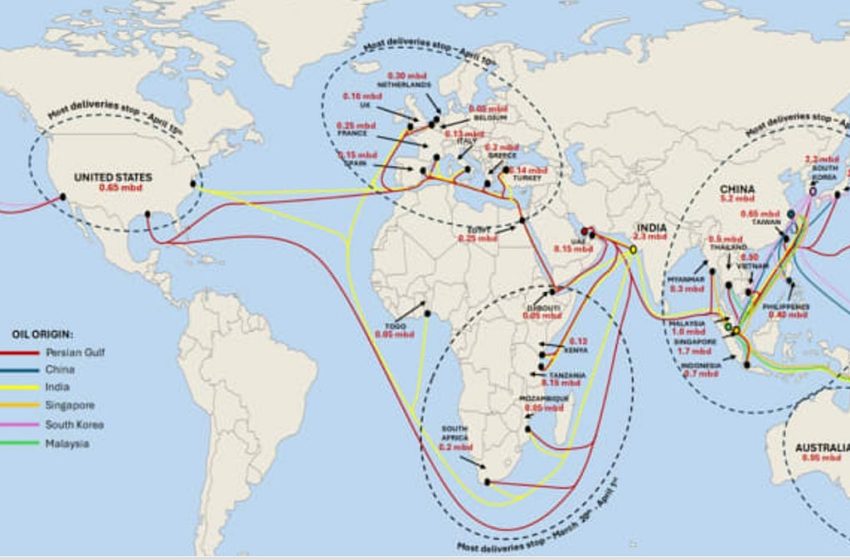

However, this grace period is about to end. The oil crisis is about to get physical. The map at the top of this post shows J.P. Morgan’s estimates of when tankers from the Gulf will stop arriving at various destinations. Deliveries to Asian markets will end this week; deliveries to Europe will end next week.

And once the crisis gets physical, there will no longer be room for jawboning the markets. Since the war began there have been several occasions on which Donald Trump has been able to talk prices down by asserting that meaningful negotiations are underway with his invisible friends the Iranian regime, but that won’t work once the oil runs out. So prices will have to rise to whatever level destroys enough demand to match it to the available supply.

PS: The United States buys little oil from the Persian Gulf, but we can expect U.S. oil prices to rise in response to shortages around the world.

So how high will oil prices get? I’ve written about this before, but I thought it might be useful to update the analysis, emphasizing how uncertain the prospects are and the real risk of extremely high prices.

There are two big sources of uncertainty. The first is that we don’t know how much oil will manage to escape the Gulf. Right now oil supply is drastically curtailed, but not by the full 20 million barrels of oil a day that used to flow through the Strait of Hormuz. The Saudis have a pipeline that lets them ship some of their oil to the Red Sea; Oman has a pipeline that takes some oil around the Strait. And Iran has been letting millions of barrels of its own oil pass. Whether all these “leakages” will continue depends on the course of the war.

Second, how high must prices rise to choke off a given amount of demand? We know from previous oil shocks that the price elasticity of demand for crude oil is low — that is, even large price increases only cause small declines in demand. But in the current crisis it matters just how low that elasticity, a number that is impossible to estimate with any precision, really is.

So, what is a reasonable range of possibilities? I’ve considered three scenarios for the disruption to oil supply: a “low disruption” scenario in which supply is reduced “only” 8 percent from normal levels, a medium scenario in which supply falls 12 percent, and a high disruption scenario in which it falls 16 percent. I’ve also considered three alternatives for the price elasticity of oil demand: “high” at 0.2, medium at 0.15, and low at 0.1.

And I assume that in the absence of this war the Brent price would be $65 a barrel. In that case I get the following matrix:

Readers should know that Robin Brooks has done a conceptually similar analysis. My numbers, however, are more alarming — and I believe that you should be alarmed.

In particular, by presenting the analysis this way, I risk conveying the impression that we should assume a moderate, medium/medium outcome. That is not at all a safe assumption.

After all, what would it take to get to my “high disruption” scenario? That’s what might happen if Iranian oil exports are cut off, say by a U.S. attack on Kharg Island, and if supply via pipelines is hindered by Iranian retaliation against other Gulf oil facilities as well as attacks by the Houthis on Red Sea shipping. That is not an outlandish possibility. It is, in fact, exactly what we should expect if the Trump administration follows through on what appear to be its current war plans.

And if oil really does go to $200 or more, it’s all too easy to envisage a full-blown global economic crisis, with an inflation surge and quite likely a recession.

Ever since this war began I’ve noticed a sharp divide in sentiment among experts. Finance and macroeconomics experts have been relatively sanguine about our ability to ride out this storm. But talk to or read energy experts — people who focus on the physical side of the oil crisis — and their hair is on fire.

I’m mostly a macroeconomist. But my hair is definitely starting to smolder.

MUSICAL CODA

My apologies

First Appeared on

Source link